Best Furniture Financing for Bad Credit: A 2026 Guide

A lot of people hit the same wall at the same time. They finally move into a new place, or they decide the old hand-me-down setup has to go, and then the credit score gets in the way. The sofa is worn out. The mattress hurts your back. The dining table doesn’t fit the family anymore. But the financing options look confusing, expensive, or built to trap you in a payment plan that never seems to end.

That stress is real. It’s also fixable.

The best furniture financing for bad credit isn’t the option with the lowest advertised payment. It’s the option that gets you the furniture your home needs without creating a bigger financial mess later. That means looking past “no credit needed” slogans and focusing on approval path, total cost, and whether the deal fits your monthly budget.

For many families in Lubbock, Hobbs, and Ruidoso, this decision sits inside a bigger rebuilding season. Maybe you’re recovering from medical bills, a job change, divorce, or a rough stretch where everything cost more than expected. If that’s you, you’re not failing. You’re making practical decisions under pressure. If broader credit rebuilding is part of your plan, this guide on how to buy land with bad credit is also worth reading because it shows the same core principle. Bad credit narrows your options, but it doesn’t erase them.

Your Dream Home Is Within Reach Even with Bad Credit

A comfortable home doesn’t start with a perfect score. It starts with a clear plan.

What people usually get wrong

Most bad-credit shoppers focus on one question first. “Can I get approved?”

That matters, but it’s not the full job. The better question is, “Can I get approved for something I can live with?” There’s a huge difference between a financing plan that helps you furnish your home and one that drains your budget month after month.

I’ve seen this pattern again and again. A family needs a sectional because the kids are sitting on the floor. A couple needs a real bed because an air mattress stopped being a temporary solution months ago. A new mover needs a dining set, a dresser, and a sofa fast because empty rooms make the whole house feel unfinished. In every case, the pressure creates urgency, and urgency makes expensive financing look harmless.

It isn’t harmless.

The goal is furniture, not financial damage

You deserve a home that feels settled. That means a sofa that fits your living room, a mattress that supports your sleep, and a dining set that makes everyday meals easier. It does not mean saying yes to the first approval screen and sorting out the consequences later.

Practical rule: If a financing option is easy to approve but hard to explain, slow down.

The right path usually comes from matching the financing type to the purchase itself. A mattress you need this week is different from a custom sectional you can plan for. A basic bedroom setup for a new apartment is different from a full-home furnishing project.

What smart shoppers do instead

They keep three priorities in front of them:

- Protect the monthly budget: The payment has to fit real life, not your most optimistic month.

- Understand ownership: In some plans, you own the furniture right away. In others, you don’t own it until every term is complete.

- Ask for total cost: Weekly or monthly payments can hide a very expensive agreement.

That’s how you turn bad-credit furniture shopping from a stressful scramble into a solid decision.

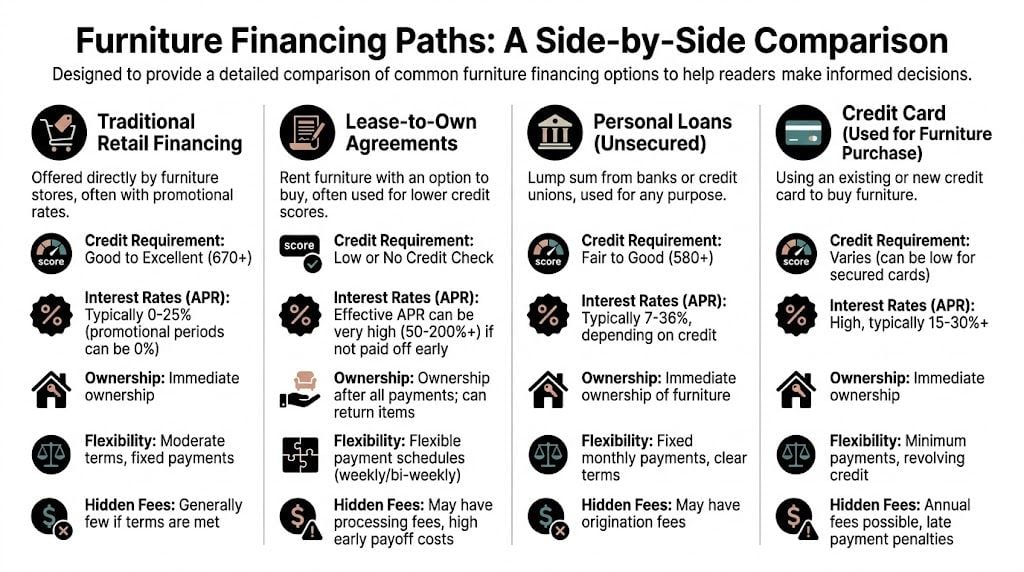

The Complete Map of Furniture Financing Options

Bad credit shoppers in Lubbock, Hobbs, and Ruidoso usually see the same words over and over: financing, no credit needed, easy approval. Those labels hide very different products. If you do not separate them, you can end up comparing a low-cost promo plan to a high-cost lease agreement as if they are the same thing.

They are not.

Retail financing through the store

Store financing is often the first place to check because it can include more than one approval path. A retailer may offer promotional financing for qualified buyers and a separate option for shoppers with weaker credit or no traditional approval.

That matters in real life. A family replacing a worn-out mattress in Hobbs may qualify for one option, while a new homeowner furnishing a living room in Lubbock may be routed to another with very different terms, fees, and ownership rules. Ask which program you are being approved for before you talk about monthly payments.

If you want to see how a local retailer lays out its choices, review these furniture financing options at Miller Waldrop.

Lease-to-own and no-credit-check programs

This category gets attention for one reason. It approves shoppers who get turned down elsewhere.

That does not make it cheap.

Lease-to-own and no-credit-check programs can solve an immediate problem, especially if your child needs a bed now or you are furnishing a home after a move. But many of these agreements cost far more over time than a standard installment loan or a promotional retail plan. You also may not own the furniture until every required payment is made under the contract.

For local shoppers in West Texas and southeastern New Mexico, total cost matters most. A low weekly payment can look manageable in the showroom and still become the most expensive option in the room.

Personal loans

A personal loan gives you cash first and ownership right away. You buy the furniture as a cash buyer, then repay the lender in fixed installments.

I like this option for households furnishing several rooms at once because the structure is cleaner. One payment is easier to track than multiple store accounts, and fixed terms make comparison easier. If your credit is damaged but your income is stable, local banks and credit unions in the region may be worth checking alongside online lenders.

If other debt is already squeezing your budget, review broader options like these best debt consolidation loans for bad credit. Reducing pressure on your monthly cash flow can make a furniture purchase safer and cheaper.

Buy now, pay later

BNPL works for small, controlled purchases. It is a poor fit for a whole-home setup unless you are disciplined.

The risk is not one plan. The risk is stacking a sofa payment, an appliance payment, and a mattress payment until your paycheck is already spoken for before groceries and utilities. Shoppers in fast-growing markets like Lubbock run into this often after a move because every room seems to need something at once.

Credit cards and secured cards

A credit card gives you immediate ownership and flexibility. It also becomes expensive fast if you carry the balance.

Use this path only if you already have available credit and a clear payoff schedule. A secured card can help in limited cases, but it usually makes more sense for smaller purchases than a full furnishing project.

Local banks and credit unions

National financing offers are not your only option. In West Texas and New Mexico, local lenders sometimes make more practical decisions because they can weigh steady employment, local banking history, and deposit relationships more directly than a national instant-approval system.

For shoppers in Ruidoso rebuilding after a setback, or families in Hobbs with solid income but a rough credit file, that local review can lead to a better long-term deal than the flashy no-credit-needed option advertised on the sales floor.

Side-by-Side Comparison of Furniture Financing Paths

If you want the short answer, here it is. The best furniture financing for bad credit is usually the cheapest option you can realistically qualify for, not the fastest one. Fast approvals are useful, but cost still wins.

Use this table first, then read the deeper breakdown below.

Furniture Financing Options at a Glance

| Financing Type | Best For | Typical Cost | Credit Impact |

|---|---|---|---|

| Retail promotional financing | Shoppers with enough credit to qualify for special offers | Can be low during promo periods, but expensive if terms are missed | May help or hurt depending on payment history |

| No-credit-needed lease-to-own | Shoppers denied elsewhere who need furniture now | Often high total cost over time | Varies by provider and structure |

| Personal loan | Shoppers who want fixed terms and immediate ownership | Depends on lender and credit profile | Payment history can matter significantly |

| Layaway | Shoppers who can wait and want to avoid debt | Down payment required, no interest debt structure | Generally not used as a credit-building tool |

| Credit card | Shoppers with available credit and a payoff plan | Can get expensive if balance carries | Revolving balance can affect utilization |

Retail financing works best when you can follow the rules

Retail financing is often the strongest option if you can qualify for the promotional terms and pay exactly as agreed. You get the furniture immediately, and the structure is familiar.

The upside is obvious. Some retailer financing includes 0% APR promotions for up to 60 months for qualifying buyers, which can be far cheaper than bad-credit alternatives when used correctly. The downside is also obvious. Miss the terms, carry the balance the wrong way, or trigger deferred interest language, and the deal can become much more expensive.

Many shoppers face issues. They remember the low payment and forget the fine print.

A promo offer is only cheap if you finish it on the promo terms.

No-credit-needed plans are accessible, but you pay for that access

Store-specific no-credit-needed programs can absolutely help people get approved. Some of these options have approval rates over 85% for scores below 600, but reported post-promotional APRs can range from 25% to 29%. By contrast, layaway requires 25% down and avoids debt and interest entirely (Credit Karma on furniture financing with bad credit).

That tells you almost everything you need to know.

No-credit-needed financing is often the right move when:

- you need essential furniture now,

- a standard credit approval isn’t realistic,

- and you have a clear early payoff strategy.

It’s a dangerous move when:

- you’re focused only on low periodic payments,

- you haven’t asked for total cost,

- or you’re financing wants instead of needs.

One local option shoppers may encounter is https://www.millerwaldrop.com/more-ways-to-pays/, which outlines payment routes available at the store level. Use any such page the same way you’d use a lender disclosure. Read it for structure, not slogans.

Personal loans are cleaner than they look

People with bad credit often skip personal loans too quickly because they assume they won’t qualify or that the process is too formal.

That’s a mistake.

A personal loan can be the most understandable option on the table. One amount borrowed. One payment. One payoff schedule. No confusion over whether you own the furniture immediately.

I like personal loans best for larger planned purchases, especially when you’re furnishing more than one room and want to avoid juggling separate financing products. They also work well for disciplined borrowers who care more about fixed terms than instant approval.

Layaway is underrated

Layaway doesn’t get enough respect because it isn’t exciting.

It’s also one of the safest tools available when the purchase can wait. You lock in the item, make payments over time, and avoid the debt spiral that can come from overextending on credit. If your budget is tight and your need isn’t immediate, layaway can be the smartest move in the room.

Credit cards are convenient, not forgiving

Using a card for a furniture purchase can be fine if you already have the line available and a short payoff horizon. It’s a poor choice if you’re going to revolve the balance for a long time.

Cards are easy to swipe and easy to underestimate. Furniture is expensive enough that one purchase can sit on your utilization for months.

My opinionated ranking

If you’re choosing based on financial health, not marketing, here’s the order I’d use:

- Promotional retail financing, if you clearly qualify and understand the terms.

- Personal loan or local credit union financing, if the payment is fixed and affordable.

- Layaway, if the purchase can wait.

- No-credit-needed financing, only when the furniture is needed now and you’ve reviewed the full cost.

- Credit cards, unless you can pay them down aggressively.

That ranking changes only when urgency changes. Need matters. A family without a bed or sofa may need access first and optimization second. But even then, you should still compare the actual cost, not just the path to approval.

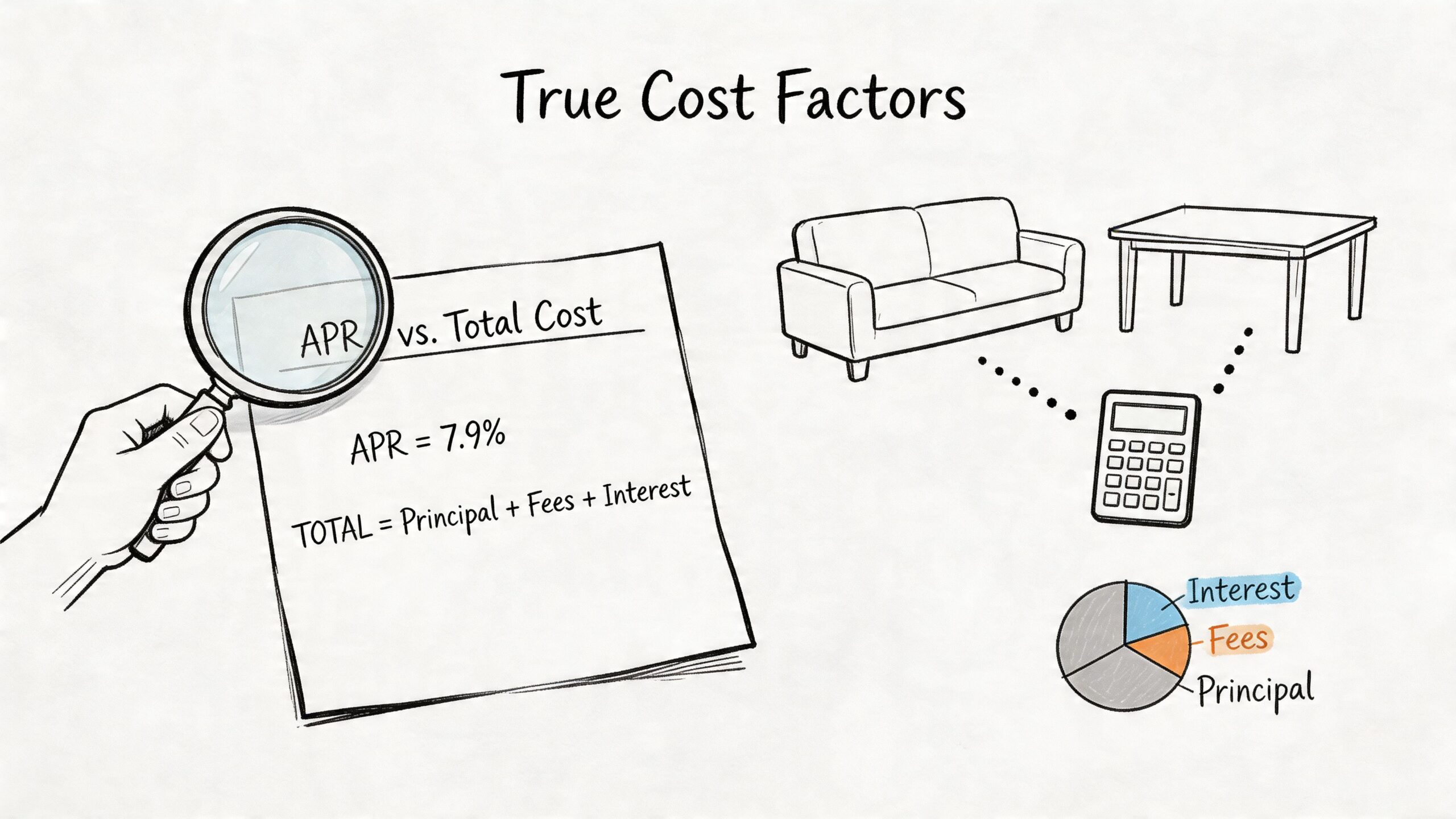

Calculating the True Cost of Your Furniture Loan

The biggest mistake bad-credit shoppers make is shopping by payment instead of shopping by total cost.

A weekly payment can look harmless. A monthly payment can look manageable. Neither tells you what the furniture will cost by the end.

The iceberg problem

The visible part of the deal is the payment amount. The hidden part is everything underneath it.

That hidden part includes:

- how long you’ll pay,

- whether the agreement is a lease or a loan,

- whether ownership is immediate,

- whether there are early payoff terms,

- and what the full repayment amount looks like.

Lease-to-own requires serious caution. While no-credit-check lease-to-own options from providers like Acima or Snap Finance are highly accessible, reporting tied to CFPB findings says their APR equivalents can average 100% to 300%, and the total cost can reach 2 to 3 times the original cash price (bestbuy-furniture.com on furniture financing and leasing).

That’s not a rounding error. That’s the whole decision.

Ask this exact question: “What is the total amount I will pay if I make every scheduled payment and do not pay early?”

If the seller or financing partner can’t answer that clearly, stop.

Questions that protect your wallet

Use this checklist before signing anything:

- What’s the cash price? You need the starting point.

- Is this a lease or a loan? Those are not interchangeable.

- When do I own the furniture? Immediate ownership and eventual ownership are different products.

- Is there an early payoff option? If yes, ask for the exact terms in writing.

- What happens if I miss a payment? You need to know before life gets messy.

- What is the full scheduled cost? This is the number that matters most.

A better way to evaluate the deal

Think in three layers instead of one.

First, decide whether the furniture is a need now or a want soon.

Second, compare the full agreement cost to the benefit of getting the item immediately.

Third, ask whether the same budget could support a different financing path with cleaner terms.

A lot of bad deals survive because people don’t force the conversation to move from “What’s your payment?” to “What’s your total cost?” Once you make that shift, expensive agreements become much easier to spot.

Financing Furniture in West Texas and New Mexico

National advice is fine until it ignores where you live.

Lubbock, Hobbs, and Ruidoso shoppers aren’t just choosing between generic online options. You’re dealing with regional lenders, local store relationships, state-specific rules, and the practical reality that many households here want to talk to a person before committing to a major purchase.

Why local context matters

National financing guides often miss how Texas and New Mexico rules shape your options. Reporting on this topic notes that Texas has finance code caps on some high-fee agreements, and that local credit unions in the region may offer furniture loans at 8% to 12% for scores as low as 550, an option many shoppers overlook when they focus only on national lease-to-own chains (Acorn Finance on furniture financing).

That’s a major practical takeaway. If you live in West Texas or Southeastern New Mexico, don’t assume the flashy national ad is your only route.

Check local institutions. Ask local stores which financing partners they work with. Ask whether there’s an in-house route, a third-party lease route, or a promotional retail route. Geography changes the answer more than most articles admit.

Why local stores can be easier to work with

A local showroom can do something a national app can’t. It can help you match the purchase to the financing path.

That matters when you’re comparing:

- a basic Ashley sofa for immediate everyday use,

- a La-Z-Boy recliner for comfort and durability,

- a Flexsteel sectional meant to anchor a family room for years,

- or a mattress setup you need delivered quickly.

A good local team can tell you which products are worth financing, which purchases are better handled with a wait-and-save plan, and whether your budget supports the item you want without forcing you into a bad agreement.

You can also use the store’s location details to decide where to shop in person across the region at https://www.millerwaldrop.com/locations/.

Local financing advice is often better because it starts with your actual room, your actual budget, and your actual town.

My recommendation for regional shoppers

If you’re in Lubbock, Hobbs, or Ruidoso, compare in this order:

- local credit union or bank option,

- store promotional financing if you can qualify,

- local store no-credit-needed route if you need furniture now,

- national lease-to-own only after you’ve asked for total cost and early payoff terms.

That order gives you the best chance of getting both the furniture and a deal you can live with.

A Practical Guide to Getting Approved for Financing

You’re standing in a showroom in Lubbock, Hobbs, or Ruidoso. The sofa your family needs is right in front of you. The only question is whether the application gets approved.

Approval usually comes down to preparation, not luck.

Bad credit puts pressure on the process, but it does not take you out of the running. The shoppers who get better results show up with the right documents, ask better questions, and apply for an amount that fits both their income and the actual value of the furniture.

What to bring before you apply

Different financing programs look for different proof. Some care heavily about credit history. Others focus more on income, residence, and payment method. If you walk in missing paperwork, you slow the process down and give the lender a reason to say no.

Bring these items:

- Proof of income: Recent pay stubs, benefit statements, or other current income records

- Identification: A valid government-issued ID

- Proof of residence: A utility bill, lease, or similar document

- Banking details: Some providers require a bank account and scheduled payments

- Your budget notes: A clear maximum monthly payment and your target total purchase amount

Bring digital copies too. A lot of avoidable denials start with a missing document, not a bad score.

How to improve your approval odds

Start smaller.

If your credit is bruised, do not apply for a full living room, bedroom, and dining room package just because the payment looks manageable on day one. In West Texas and southeastern New Mexico, the smarter move is to finance the pieces that solve the immediate problem first. A mattress for better sleep. A sofa that seats the family. A recliner for a recovery need.

Then improve your odds with a few disciplined steps:

- Apply for what you need now. Smaller approvals are easier to get and easier to repay.

- Put money down if you can. Even a modest down payment can reduce risk for the lender and lower your long-term cost.

- Ask which type of financing you are being offered. Store credit, promotional financing, lease-to-own, and no-credit-needed programs are very different products.

- Ask for the early payoff terms in plain language. This matters a lot if you expect your income to improve or plan to pay the balance off ahead of schedule.

- Keep the application accurate. Income, address, and employment mismatches create delays and can trigger a denial.

One more rule. Do not let approval become the goal. The goal is getting the furniture your household needs at a cost you can live with six months from now.

What to say when talking to financing staff

Be direct.

Tell them what room you are furnishing, which pieces are required today, and the highest monthly payment your budget can absorb without missing groceries, utilities, or your car payment. That gives the financing staff something useful to work with.

Say it like this:

- I need a sofa and mattress, not a full-house package.

- My max monthly payment is $X.

- I want to know the total cost, not just the approval amount.

- Show me the option with the lowest full payoff cost if I pay on schedule.

- If this is lease-to-own or no-credit-needed financing, explain the early purchase option before I sign.

That last line is the one I recommend most for shoppers in Lubbock, Hobbs, and Ruidoso. Local buyers often focus on getting approved fast, which is understandable. But the stronger move is asking what the furniture will cost by the end. That single question can save your family from paying far more than the ticket price.

From Financing to Furnishing Your Miller Waldrop Showroom Guide

Good financing is only useful if it leads to furniture that solves the problem in your home.

That’s why your next step shouldn’t be another random online application. It should be matching your budget to the right category and the right piece.

Start with the room that affects daily life most

For most families, that’s the living room or bedroom.

If your current setup is causing the most frustration in the living room, start with a durable centerpiece and build around it. A sectional often makes more sense than piecing together multiple smaller seats, especially for families, movie nights, or homes where the living room does a lot of work every day. If that’s your priority, explore Flexsteel sectionals and focus on size, cushion feel, and long-term use.

If sleep is the bigger issue, move the mattress to the top of the list. Better sleep improves everything else in the house.

Use financing as a tool, not a permission slip

That shift matters.

Financing should help you get the right sofa, recliner, dining set, or mattress at the right time. It shouldn’t tempt you into buying a room package your budget can’t support. The strongest shoppers stay focused on function first, then style, then stretch upgrades only if the numbers still work.

One local option for shoppers comparing payment routes is Miller Waldrop Furniture & Decor, which offers furniture and mattress selections across brands like Flexsteel, La-Z-Boy, Ashley, Serta, and Beautyrest along with financing pathways tied to store purchases.

A smart showroom visit looks like this

Walk in with:

- a room measurement,

- a target monthly payment,

- a short list of must-have pieces,

- and the questions from this guide about ownership and total cost.

That turns the visit into a planning session instead of a pressure moment.

Common Questions on Bad Credit Furniture Financing

Will applying lower my credit score even more

Sometimes it can, depending on the application type. That’s why you should ask whether the financing path involves a traditional credit check or a no-credit-needed review process before applying.

What if I’m denied

Don’t panic and don’t jump straight to the most expensive option. Ask whether there’s another route through the same store, reduce the purchase size, or consider layaway for non-urgent items.

Can I get approved if I’m new to the area or just started a job

You may still have options. Approval often depends on the financing type, your current income, and the documentation you can provide. Being prepared matters more than being established for years.

Is lease-to-own always a bad idea

No. It’s a tool. It becomes a bad idea when you ignore the total cost, don’t understand the ownership terms, or use it for purchases that could wait.

If you’re ready to turn this into a real plan, visit Miller Waldrop Furniture & Decor. Bring your room measurements, your target payment, and your priority list. Then use the showroom, financing options, and product selection as tools to choose furniture that fits your family, your space, and your budget with clarity.